The US Auto Industry Doesn’t Have a Supply Problem. It Has a Demand Problem.

The US Auto Industry Doesn’t Have a Supply Problem. It Has a Demand Problem.

By Warren Browne

The light vehicle market has been going through a significant transformation since last June. Starting in the third quarter of 2022, the demand-supply structure of the market moved from a supply shortage into a serious demand problem that will have marketing teams scrambling to fix it.

The vehicle market has been supply-constrained over the past two years. That’s not new information. What seems odd is that many CEOs are still using supply constraints as an excuse for not meeting sales targets or earnings objectives.

Memo to the board of directors: Those days are over. There are certainly pockets of supply constraints when looking at specific models. And the level of inventory is not ideal for consumers who want to roam the lots for the right vehicle and haggle on price. However, these minor supply problems are now overwhelmed by the fact that the fundamental economics driving the vehicle market have turned very sour.

Rising Rates and Slowed Growth

The demand problem started when vehicle price increases tried to keep pace with soaring inflation and dealers were looking for more than just MSRP. As the Federal Reserve took measures to slow inflation, interest rates began increasing rapidly from their dormant state of the past two years, to where the current U.S. prime rate is the highest in 16 years. To compensate, some consumers went to seven-year loans, perhaps forgetting that they were not taking out a home mortgage. Yikes!

Economic growth also faltered. U.S. real gross domestic product declined in the first two quarters, and will close the year with growth under 1.5%. Consumers just don’t like to spend money on durable goods in that type of environment.

That was the good news. The environment supporting vehicle sales will get worse in 2023. Interest rates will continue to rise, albeit slower than the pace last year. Economic growth will be lower than last year in the United States, Canada and Mexico.

One hope for an increase in light vehicle sales this year is if a significant number of customers come to the dealer and buy what they ordered last year. This prospect seems difficult to imagine, especially if they were betting on a good price for their used vehicle.

Inventory Up as Sales Languish

Will there be longer waiting times for customer orders? Yes, especially for battery-electric models that are in a startup phase. Yet recent inventory growth is one indicator that overall supply constraints are gone. Inventory at the dealer and regional supply centers grew to 2.28million units last year, up from 1.38million at the beginning of the year. Further growth to 3.0million units will be achieved by the end of this year, roughly 60 days’ supply.

An additional indicator is assembly plant capacity utilization. Overall utilization in 2022 was 74% of 19.8 million units of useable capacity. Seventeen plants operated above 85-90% utilization, a benchmark that indicates significant profit generation. Importantly, 2022 actual production reached 86% of 2018 levels, the last market peak.

Unfortunately, the industry will experience a vehicle demand problem that will last for the next six quarters. Anticipated 2023 sales of 17.18 million will be helped, somewhat, by pent-up demand. But sales will languish at COVID-era levels and be three million units below trend.

Conversely, production will continue to roll on. Manufacturers will produce enough vehicles to satisfy USMCA demand and exports, and have some left over to grow dealer inventory.

Numbers Trending Downward

Our pessimistic view is derived by separating the influence of core demand drivers from the actual sales forecast—which is further influenced by supply and incentives.

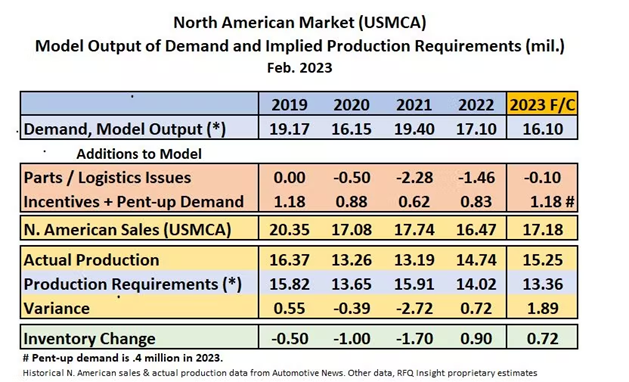

The table below outlines expected demand in North America and our final sales forecast including estimated incentives.

Warren Browne Chart

The starting point is vehicle demand given economic and employment growth, interest rates and performance of the stock market (wealth factor). The result is expected demand of 16.1 million in 2023—a million units below last year. This estimated demand results in production requirements of 13.36 million, or slightly above actual production during COVID.

The situation back then was completely different, however. Actual 2020-21 production was constrained by parts supply, labor shortages and logistics issues. Thus, production was below what the market would have required to hit the sales number. The only way sales hit 17 million units during 2020-21 was through 2.7 million units of inventory reductions and moderate levels of incentives.

This supply-constrained environment was reversed in 2022 when actual production of 14.74 million was greater than requirements of 14.02 million. The production level in 2023 will be above demand requirements and continue to build dealer Inventory.

No More Excuses

So where does that leave us this year? We do not envision any serious parts issues or permanent plant closures. Plant closures do not look good in a labor-contract year. In fact, overall plant capacity will increase to 19.6 million, including more battery-electric allocation. (Stellantis’ Belvidere plant is mothballed). The crutch of a “supply shortage” excuse has been removed.

The real issue is how OEMs and dealers will manage the demand problem. Will their current behavior change when it comes to margins and discounts? While marketing teams may vote “yes” as they scramble to fix the demand problem, CFOs may not want to move that fast.

The tea leaves indicate a continuation of the 2022 strategy: profits before sales. The investment and engineering expense of the electric revolution is heavy enough and will force this “profit strategy.” This means incentives, except those provided by taxpayers through the Inflation Reduction Act, will be lower than 2022 levels. Likewise, price increases will continue close to inflation levels.

The COVID-era may have produced unintended consequences for mainstream consumers looking for a big deal: The next big incentive fight will not return to town for some time. Manufacturers and dealers have learned that less is more, and they can prosper at North American sales levels of 17 million. Production workers will have to get used to that reality as well.

Source :